You’ve got Bitcoin, Ethereum, or stablecoins sitting in your wallet. Now you want to actually use that money, pay rent, buy groceries, or just have cash in your bank account. That’s where off-ramps come in.

A crypto off-ramp is any method that converts your cryptocurrency into traditional money (fiat) that you can spend in the real world. Understanding your off-ramp options matters because fees, speed, and limits vary wildly between methods.

This guide explains what off-ramps are, compares the main options, and helps you choose the right one for your situation.

Key Takeaways

- An off-ramp converts crypto to fiat currency (USD, EUR, etc.)

- Main options: exchanges, crypto cards, P2P platforms, and crypto ATMs

- Centralized exchanges are cheapest but slowest (bank transfers take days)

- Crypto debit cards offer instant spending without converting to bank first

- All off-ramps may trigger taxable events, track your transactions

What is a crypto off-ramp?

In crypto terminology:

- On-ramp = Buying crypto with fiat (getting into crypto)

- Off-ramp = Selling crypto for fiat (getting out of crypto)

When you off-ramp, you’re converting digital assets back into traditional currency. This could mean:

- Selling BTC on Coinbase and withdrawing to your bank

- Spending crypto with a debit card at a store

- Selling USDT to someone locally for cash

- Using a Bitcoin ATM to withdraw dollars

The method you choose affects how much you pay in fees, how fast you get your money, and how much paperwork is involved.

Types of crypto off-ramps

1. Centralized Exchanges (CEX)

The most common off-ramp. Sell your crypto on an exchange like Coinbase, Kraken, or Binance, then withdraw fiat to your bank account.

How it works:

- Deposit crypto to your exchange wallet

- Sell for USD/EUR/GBP

- Withdraw to linked bank account

Pros:

- Lowest fees (0.1-1% trading fee)

- High liquidity (good prices)

Cons:

- Bank transfers take 1-5 business days

- Requires full KYC verification

- Your funds are on a centralized platform (you don’t owned it)

- Transfer / withdraw limits

- Additional verifications

Best for: Beginners, users who don’t need money instantly

Popular exchanges: Coinbase, Kraken, Binance, Gemini

2. Crypto debit cards

A crypto debit card converts your crypto to fiat at the moment of purchase. You spend crypto directly, no need to sell on an exchange first.

How it works:

- Load crypto onto your card account

- Swipe or tap at any Visa/Mastercard merchant

- Card provider converts crypto to fiat instantly

- Merchant receives regular payment

Pros:

- Instant spending (no waiting for bank transfers)

- Works at millions of merchants worldwide

- Often lower KYC than exchanges

Cons:

- Conversion fees (0-2.5% depending on provider)

Best for: Daily spending, instant access, users who want to avoid bank transfers

Popular cards:

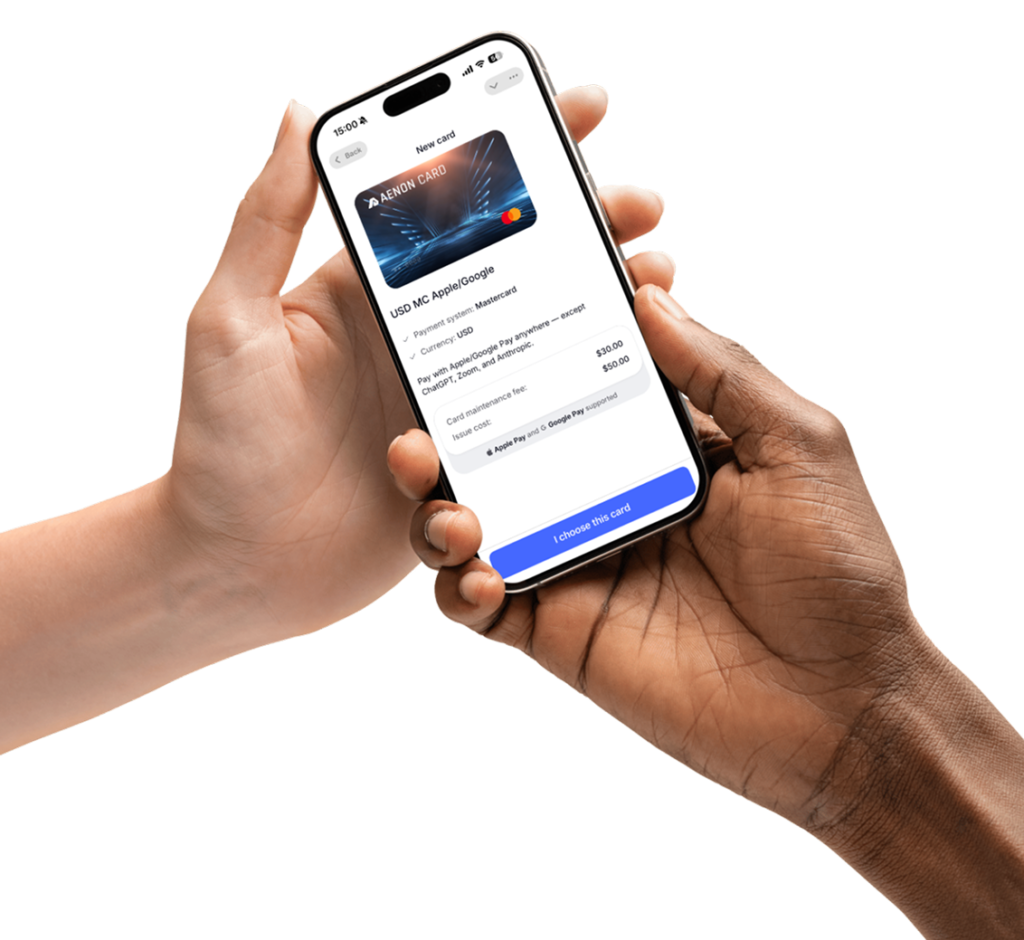

- Aenon Card: Virtual card only, no physical/ATM option, accessible via Telegram

- Crypto.com Card: Virtual + physical, ATM withdrawals available

3. Peer-to-Peer (P2P) Platforms

Sell crypto directly to another person. The platform acts as escrow to protect both parties.

How it works:

- List your crypto for sale (or find a buyer)

- Agree on price and payment method

- Platform holds crypto in escrow

- Buyer sends payment (bank transfer, PayPal, cash, etc.)

- You confirm receipt, crypto releases to buyer

Pros:

- Flexible payment methods (including cash)

- Often better rates than exchanges

- More privacy options

- Works in countries without exchange access

Cons:

- Slower (requires finding a buyer)

- Scam risk if not careful

- Prices can be worse in low-liquidity markets

Best for: Privacy-focused users, those in restricted countries, cash transactions

Popular platforms: Paxful, Bisq, LocalBitcoins (now closed), Binance P2P

4. Crypto ATMs

Physical machines that let you sell crypto for cash. Find one, scan your wallet, and withdraw bills.

How it works:

- Find a crypto ATM that supports selling (not all do)

- Verify your identity (phone, ID, or both)

- Send crypto to the ATM’s address

- Receive cash once transaction confirms

Pros:

- Get physical cash immediately

- No bank account needed

- Available 24/7

Cons:

- Very high fees (5-15% typical)

- Low withdrawal limits ($200-$500 without ID)

- Not available everywhere

- Must wait for blockchain confirmations

Best for: Emergency cash needs, unbanked users, small amounts

Find ATMs: CoinATMRadar.com

Off-ramp comparison: fees, speed, and limits

| Method | Typical Fees | Speed | Limits | KYC Required |

|---|---|---|---|---|

| Exchange → Bank | 0.1-3% | 1-5 days | $50K+/day | Full |

| Crypto debit card | 0-3.5% | Instant | $10K-500k/month | Light (with Aenon Card) |

| P2P Platform | 0-3% | Hours to days | Varies | Optional |

| Crypto ATM | 5-15% | 10-60 min | $200-$10K | Light-Full |

How to choose the right off-ramp

For everyday spending

Use: Crypto debit card

Don’t bother selling on an exchange and waiting for bank transfers. A crypto card lets you spend directly at any merchant, worldwide and privately (with Aenon Card). The 1-3.5% fee is worth the convenience.

Tax implications of off-ramping

Important: Converting crypto to fiat is a taxable event in most countries. When you off-ramp, you’re technically “selling” your crypto, which may trigger:

- Capital gains tax if your crypto appreciated in value

- Capital losses (potentially deductible) if it decreased

This applies to:

- Selling on an exchange

- Spending with most of crypto debit card

- P2P sales

- ATM withdrawals

Tip: Track every transaction. Tools like Koinly, CoinTracker, or your exchange’s tax reports can help calculate your obligations.

Common off-ramp problems (and solutions)

Bank blocks crypto-related deposits

Some banks flag or freeze accounts receiving funds from crypto exchanges.

Solutions:

- Use a crypto-friendly bank (Revolut, N26, Monzo)

- Use a crypto debit card instead of bank transfers

- Call your bank in advance to explain the incoming transfer

Exchange withdrawal limits too low

New accounts often have restricted withdrawal limits.

Solutions:

- Complete higher verification tiers

- Build account history over time

- Use multiple exchanges for larger amounts

Long confirmation times

Bitcoin transactions can take 10-60 minutes to confirm.

Solutions:

- Use stablecoins (USDT, USDC) for faster settlements

- Choose networks with faster confirmations (Ethereum L2s, Solana)

- Pay higher network fees for priority processing

Frequently asked questions

What is the cheapest way to off-ramp crypto?

Selling on a centralized exchange and withdrawing via bank transfer is typically cheapest (0.1-1% total fees). However, it takes 1-5 days and it’s centralized. For instant access, crypto debit cards cost slightly more (1-3.5%) but eliminate the wait and keep the control and privacy.

Can I off-ramp crypto without KYC?

Limited options exist. P2P platforms allow some no-KYC trades, and crypto ATMs often allow small withdrawals ($200-$500) with just phone verification. For larger amounts, KYC is generally required by law. With Aenon Card you only need a light KYC at registration.

How long does it take to convert crypto to cash?

It depends on your method:

- Crypto debit card: Instant (at point of sale)

- Crypto ATM: 10-60 minutes (waiting for confirmations)

- P2P: Hours to days (depends on buyer)

- Exchange to bank: 1-5 business days

Do I pay taxes when I off-ramp?

Yes, in most jurisdictions. Converting crypto to fiat is considered a disposal, triggering capital gains (or losses) based on your cost basis. Consult a tax professional for your specific situation.

Final thoughts

Off-ramping crypto doesn’t have to be complicated. Your choice depends on three factors: how much, how fast, and how much you’re willing to pay in fees.

- Large amounts, no rush: Use an exchange → bank transfer (lowest fees)

- Everyday spending: Use a crypto debit card (instant, convenient)

- Privacy/flexibility: Use P2P platforms (more options, more risk)

- Emergency cash: Use crypto ATMs (fast but expensive)

For most people, a crypto debit card is the simplest off-ramp for regular use. You skip the exchange-to-bank dance entirely and spend crypto directly wherever cards are accepted.

Want the easiest and safest off-ramp for your crypto? Aenon Card lets you spend stablecoins instantly at any store (physical or online) with Apple Pay / Google Pay. No bank transfers required. It’s a virtual card optimized for privacy.