Looking for the best crypto debit card to spend your Bitcoin, Ethereum, or stablecoins? You’re not alone. The problem is there are now a dozen options out there, each with different fee structures, KYC requirements, and limitations that aren’t obvious until you’ve already signed up.

This guide compares six crypto debit cards and breaks down what actually matters: which ones charge hidden fees, which require full identity verification (vs. just an ID selfie), and which work outside the US and EU. No fluff, just honest tradeoffs.

What actually matters when picking a crypto debit card

How much verification do they want?

KYC ranges from “upload a selfie with your ID” to “provide proof of address, bank statements, and your mother’s maiden name.” If you’ve ever had a bank freeze your account because you bought Bitcoin, you probably care about this.

Fees to watch

The issuance fee is the easy one to spot ($0–$100 upfront). The ones that bite you later:

- Conversion spread when spending crypto (0.5%–2%)

- ATM fees after you hit the free limit (usually 1%–3%)

- FX markup when spending in a different currency (0%–2.5%)

- Monthly maintenance fees (most claim $0, but check the fine print)

Which cryptos can you actually spend?

Some cards only support BTC and ETH. Others take stablecoins like USDT and USDC, which is more practical if you don’t want your coffee purchase to cost $4.50 or $6.20 depending on when the transaction clears.

Virtual vs. physical

Virtual cards show up instantly and work with Apple Pay and Google Pay. Physical cards take 1–3 weeks to arrive but work at ATMs.

Cashback is usually a trap

Advertised rates go up to 10%, but many require staking proprietary tokens (which can tank in value) or are paid in tokens nobody wants.

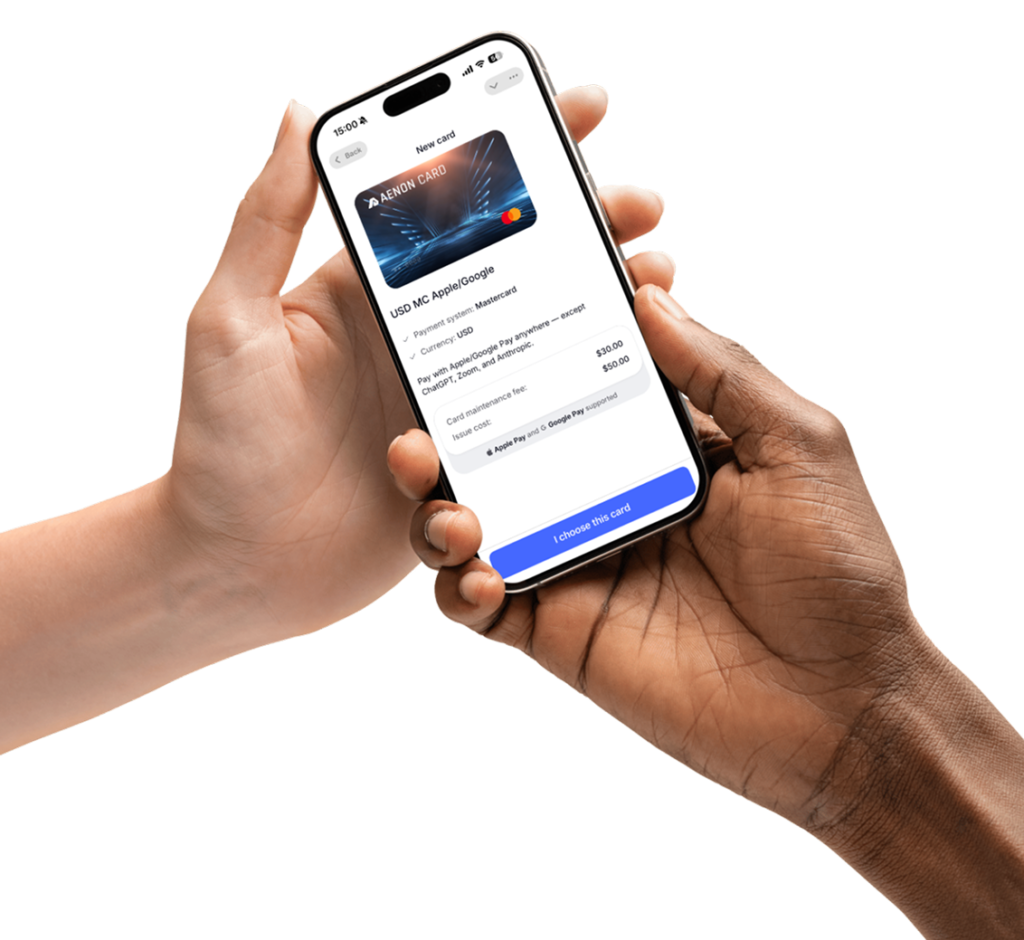

Aenon Card

Type: Virtual Mastercard

Where it works: 130+ countries

KYC: Basic info only

Supported crypto: USDT, USDC on Ethereum, BNB Chain, Tron, Polygon, Solana

Aenon Card is for people who want a crypto card without a 3-day verification process. You sign up through a Telegram bot, provide basic information, and get a virtual card in about 2 minutes. No proof of address. No video call.

The card works with Apple Pay and Google Pay, supports 5 blockchain networks, and has no monthly fees. You top up with stablecoins, which means no price volatility between when you load the card and when you spend.

The catch: No physical card, no cashback.

Who should use it: Digital nomads, privacy-focused users, or anyone who’s been burned by banks asking too many questions about their crypto activity.

Get your virtual card in minutes: @AenonWalletBot on Telegram

Crypto.com Card

Type: Visa Debit

Where it works: Global (tier-dependent)

KYC: Full

Supported crypto: 30+ cryptocurrencies

The metal cards look nice and the perks are real: Spotify rebates, Netflix rebates, airport lounge access. But you need to stake CRO tokens to get the good stuff. The entry tier (Ruby) requires $400 worth of CRO. The Obsidian tier requires $400,000.

The catch: Your staked CRO is locked. If CRO drops 50%, your stake is worth half as much and you still can’t touch it.

Who should use it: People who are already holding CRO and plan to keep holding it.

Nexo Card

Type: Mastercard (credit-style)

Where it works: EU/EEA, UK

KYC: Full

Supported crypto: 40+ cryptocurrencies

This one’s different. Instead of selling your crypto to spend, you borrow against it. Your BTC or ETH stays in your account earning interest (or at least holding its value), and you spend borrowed fiat.

Up to 2% cashback paid in NEXO tokens, or 0.5% in Bitcoin. Up to €2,000/month in free ATM withdrawals.

The catch: It’s a loan. If your collateral drops in value, you could face liquidation. Interest rates depend on your tier.

Who should use it: People who think their crypto will appreciate and don’t want to trigger a taxable sale every time they buy groceries.

Source: Nexo card page

Bybit Card

Type: Mastercard Debit

Where it works: EU/EEA

KYC: Full

Supported crypto: EUR-settled

Up to 10% cashback, which is the highest on this list. Auto-savings feature earns up to 8% APY on idle funds. No annual fee.

The catch: 2% ATM fee. EU only. You need to be a Bybit user already.

Who should use it: Active Bybit traders in Europe who want maximum cashback.

Source: Bybit help center

RedotPay

Type: Visa Debit

Where it works: 175+ countries

KYC: Tiered (light to full)

Supported crypto: USDT, USDC

RedotPay’s main advantage is availability. If you’re in Southeast Asia, Africa, or Latin America, where most other cards don’t operate, this might be your only option.

Tiered KYC means you can start with basic verification for lower limits, then upgrade if needed.

The catch: 1.2% FX fee, 2% ATM fee, physical cards cost up to $100 to issue.

Who should use it: International users in regions where Coinbase and Crypto.com don’t ship cards.

Source: RedotPay help center

Wirex

Type: Visa Debit

Where it works: EU/EEA, UK, select countries

KYC: Full

Supported crypto: 37+ cryptocurrencies

Wirex supports more altcoins than most competitors. If you’re holding DOGE, SHIB, or something obscure, you might actually be able to spend it here.

Up to 8% cashback, but it’s paid in WXT (Wirex’s token).

The catch: 1% top-up fee. Cashback in a token that might depreciate. Customer support has mixed reviews.

Who should use it: People with diverse crypto portfolios who want to spend altcoins directly.

FAQ about crypto debit card

What is a crypto debit card?

A card that lets you spend crypto anywhere Visa or Mastercard is accepted. The card converts your crypto to local currency at purchase time, so the merchant gets normal money.

Do I pay taxes when spending crypto?

In most countries, yes. Spending crypto counts as selling it, which can trigger capital gains tax. Stablecoins might be treated differently since there’s no price appreciation. Talk to a tax professional.

What’s the difference between a crypto debit card and credit card?

Debit cards spend your existing balance. Credit cards (like Nexo) let you borrow against your crypto. You keep the crypto but take on debt.

Find your best crypto debit card

There’s no “best” card for everyone. If you want fast setup with minimal verification, a human and reactive support, Aenon Card gets you spending in minutes.

The common thread: all of these are better than sending crypto to an exchange, converting to fiat, withdrawing to a bank, and then spending from there. That takes days. These cards take seconds.

Get your Aenon Card via Telegram!

Have more questions? Check our FAQ or learn more about Aenon Card.

Cryptocurrency involves risk. Card terms change. This is informational content, not financial advice.